Bitcoin Price Prediction – A High-Dimensional Machine Learning Approach

Name

Qitong Cao

Major

Applied Mathematics and Computational Science

Class

2022

About

Signature Work Project Overview

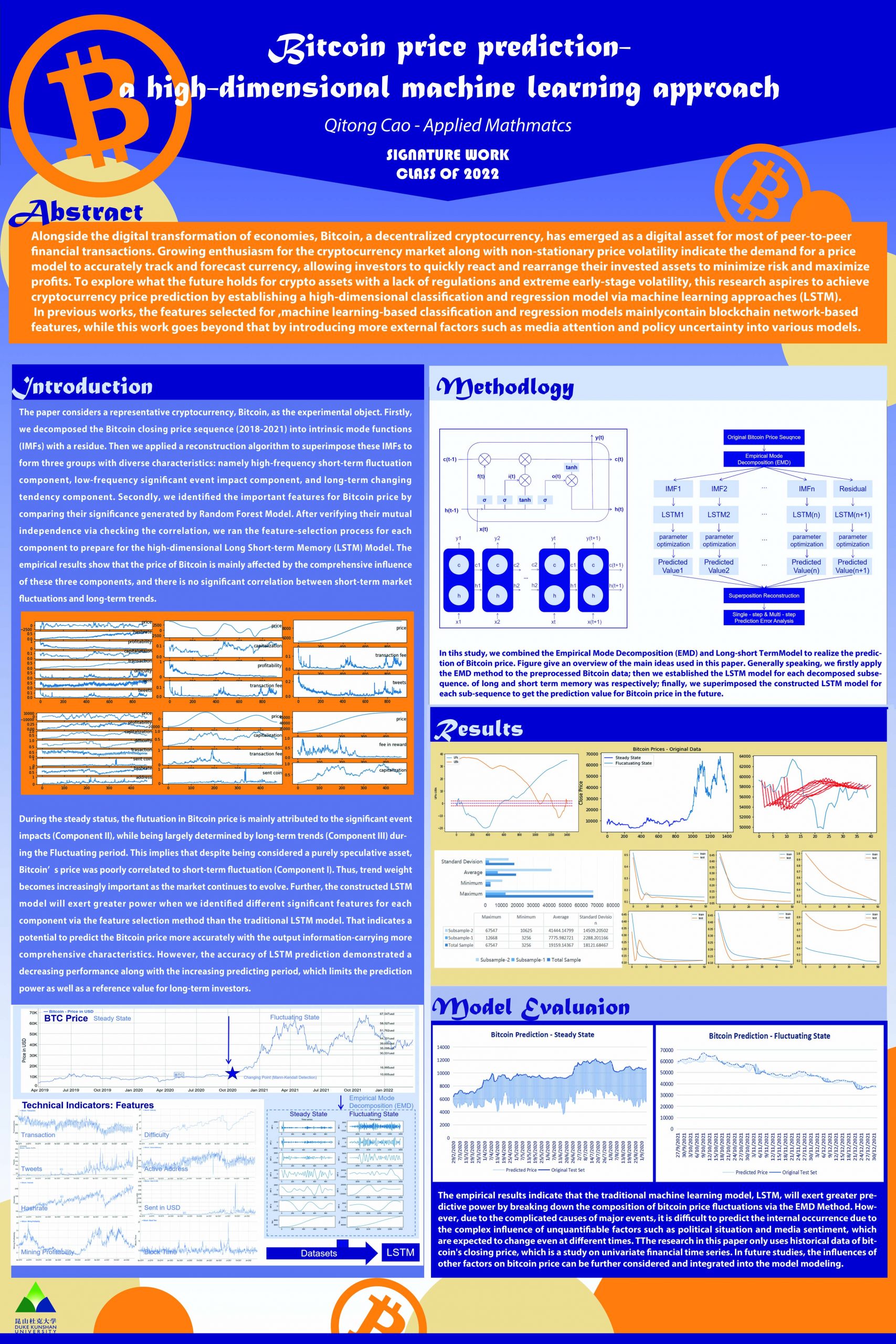

Nowadays, alongside the digital transformation of economies, Bitcoin, a decentralized cryptocurrency, has emerged as a dominant digital asset for peer-to-peer financial transactions with growing attention. However, it is difficult to manage the evaluation due to the cryptocurrency’s immeasurable intrinsic value and non-stationary price volatility. Thus, there lack of relevant financial models for bitcoin evaluation and prediction. To fill the blank in this area and to update the traditional financial model in the face of technological innovation and digitalization, this signature work’s purpose is to construct an evaluation model to assess the future price of the cryptocurrency so that to provide theoretical support and give reasonable suggestions for investors to make investments in the ongoing prevalent crypto-market in both the short term and the long term.

The empirical research shows that although bitcoin is generally regarded as purely speculative, short-term fluctuations are not the dominant factor in its price. With the continuous development of the Bitcoin market, the impact of significant events is decreasing, and the component of the long-term trend is growing decisive, while short-term fluctuations still have little impact. The research results of this paper are meaningful for investors to have a deeper understanding of the mechanism behind bitcoin price fluctuations, to timely adjust investment strategies and reduce investment risks in the complex and changeable bitcoin market.