I’m a senior student majoring in data science. I’m planning on doing graduate studies in computer engineering in the US

Signature Work Project Overview

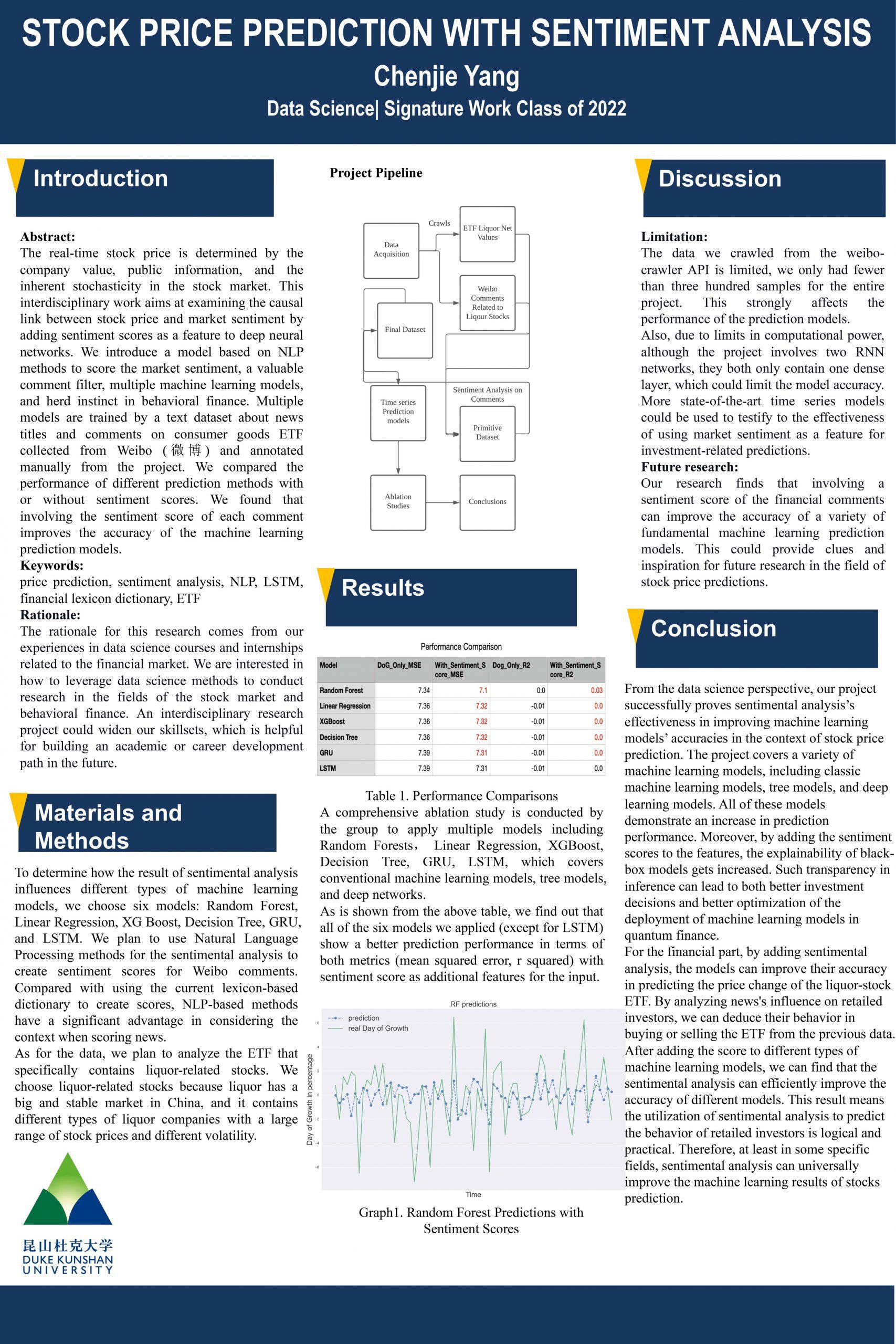

The real-time stock price is determined by the company value, public information, and the inherent stochasticity in the stock market. This interdisciplinary work aims at examining the causal link between stock price and market sentiment by adding sentiment scores as a feature to deep neural networks. We introduce a model based on NLP methods to score the market sentiment, a valuable comment filter, multiple machine learning models, and herd instinct in behavioral finance. Multiple models are trained by a text dataset about news titles and comments on consumer goods ETF collected from Weibo (微博) and annotated manually from the project. We compared the performance of different prediction methods with or without sentiment scores. We found that involving the sentiment score of each comment improves the accuracy of the machine learning prediction models.