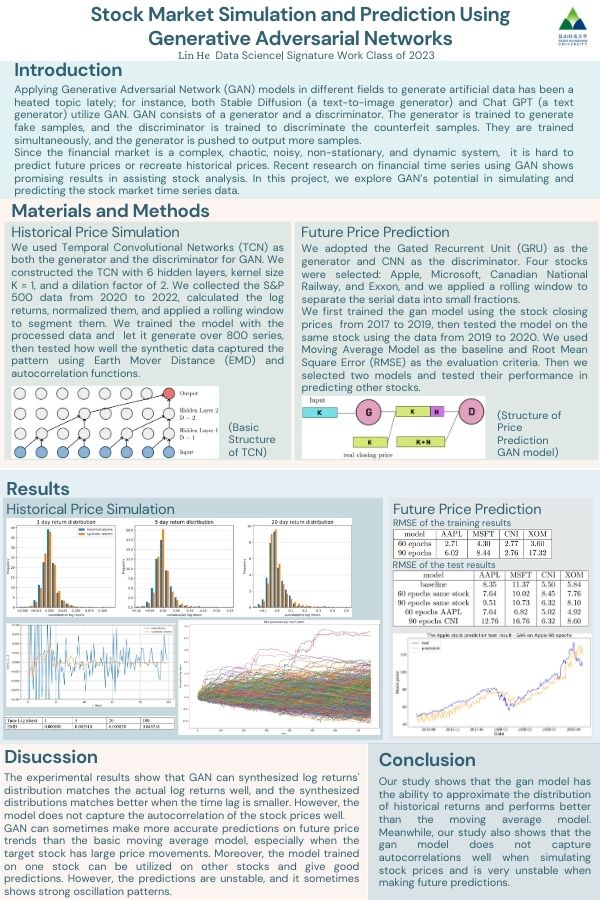

Applying Generative Adversarial Network (GAN) models in different fields to generate artificial data has been a heated topic lately. In this project, we explore GAN’s potential in simulating and predicting stock market time series data. We apply the GAN model with Gated Recurrent Unit (GRU) as the generator, Convolutional Neural Network (CNN) as the discriminator to predict future prices, and the GAN model with Temporal Convolutional Network (TCN) structures as both the generator and the discriminator to simulate historical prices. This study shows that the GAN model has the ability to approximate the distribution of historical returns and the potential to perform better than the moving average model. Extensive experiments show that the model trained on one stock can be used to predict the prices of other stocks, even when the companies are in different businesses. Meanwhile, this study also shows that the GAN model does not capture autocorrelations well when simulating stock prices and is very unstable when making future predictions.