Analysis of black swan event’s impact on Markowitz portfolio in Chinese stock market

Name

Letao Ouyang

Major

Applied Mathematics and Computational Science

Class

2023

About

Letao Ouyang is a senior student majoring in Applied Mathematics at Duke Kunshan University. He is interested in both mathematics and finance.

Signature Work Project Overview

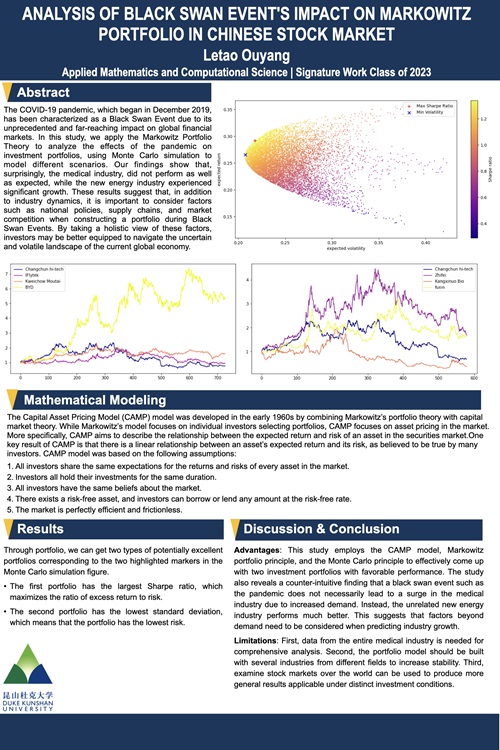

The COVID‐19 pandemic, which began in December 2019, has been characterized as a Black Swan Event due to its unprecedented and far‐reaching impact on global financial markets. In this study, we apply the Markowitz Portfolio Theory to analyze the effects of the pandemic on investment portfolios, using Monte Carlo simulation to model different scenarios. Our findings show that, surprisingly, the medical industry, did not perform as well as expected, while the new energy industry experienced significant growth. These results suggest that, in addition to industry dynamics, it is important to consider factors such as national policies, supply chains, and market competition when constructing a portfolio during Black Swan Events. By taking a holistic view of these factors, investors may be better equipped to navigate the uncertain and volatile landscape of the current global economy.