Portfolio Optimization: Investment Portfolio of S&P 500 Index Constituent Stocks Optimization: Strategy Decision and Portfolio Finding

Name

Guang Yang

Major

Applied Mathematics and Computational Sciences

Class

2024

About

My name is Guang Yang. I am from class of 2024. My major is Applied Mathematics, and my signature work is related to portfolio optimization.

Signature Work Project Overview

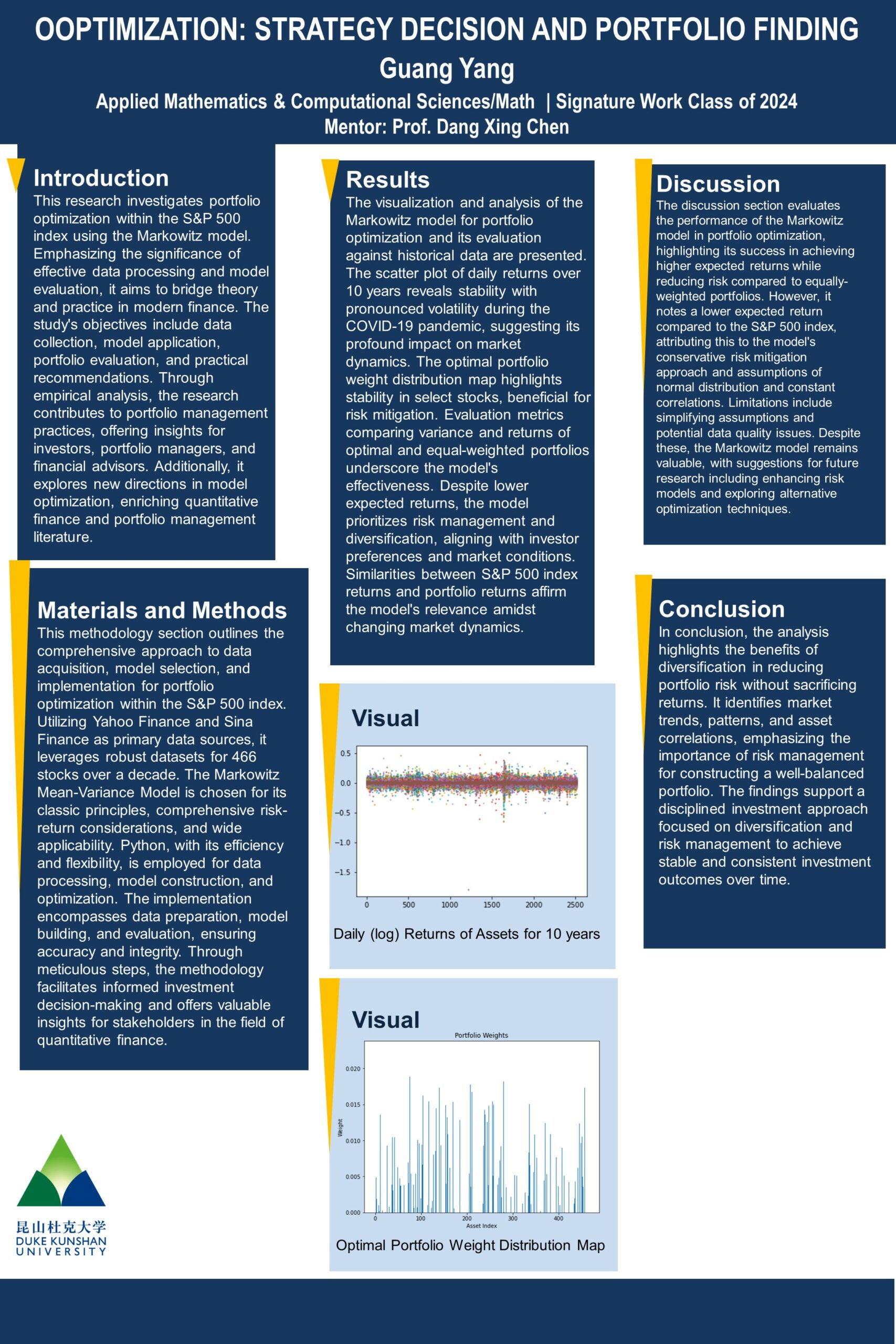

The SW investigates portfolio optimization using the Markowitz model, aiming to assess its efficacy in achieving optimal asset allocations. Through historical asset return data analysis, portfolios are constructed and optimized using mathematical optimization techniques. The study compares the variance and expected returns of these optimized portfolios with equally-weighted portfolios. Results indicate that the Markowitz model achieves higher expected returns while mitigating portfolio risk, highlighting its effectiveness in diversification. However, it’s observed that the optimized portfolio’s expected return may be lower than the market index average, suggesting limitations in maximizing returns. This underscores the significance of balancing risk and return in portfolio management decisions. The study emphasizes the need for further research to refine portfolio optimization techniques, addressing potential limitations of the Markowitz model. Overall, it contributes to the understanding of portfolio management strategies, emphasizing the importance of risk-return trade-offs for achieving optimal investment outcomes in dynamic market conditions.