SIMULATING STOCK PRICES USING GEOMETRIC BROWNIAN MOTION: A TEST TO THE OPTION PRICING THEORY FROM CHINESE COMPANIES

Name

Yuanzhi Lei

Major

Applied Mathematics and Computational Science

Class

2023

About

I am a student from Duke Kunshan University who majored in Applied math and Computational Science. I was born in Shanghai and Grew up in Beijing.

Signature Work Project Overview

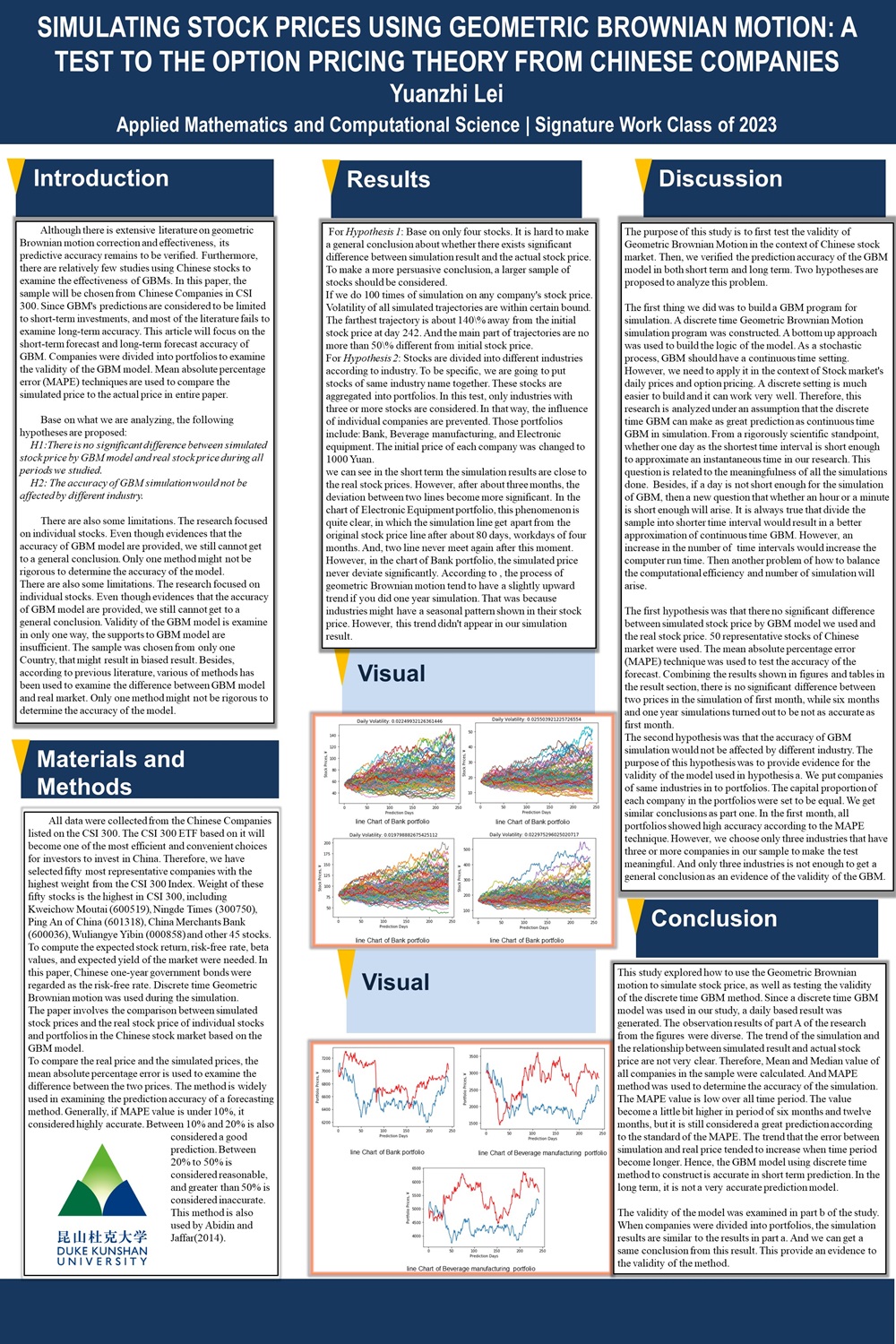

This study used the discrete-time method to construct the Geometric Brownian motion,

and use the technique to simulate the path of the stock price. The study sample was

based on the most weighted Chinese companies in the CSI 300 index. 50 Companies

were chosen. Daily data were obtained from March 12th, 2022 to March 13th, 2023.The

result shows that the Discrete-Time Geometric Brownian motion can predict the actual

stock price accurately in the short term. As the period of simulation become longer, the

prediction result becomes increasingly inaccurate. Simulations provide support to the validity of the GBM

models after dividing companies into portfolios.